Checks from the Government

by Jennifer Leach Associate Director, Division of Consumer and Business Education, FTC

As the Coronavirus takes a growing toll on people’s pocketbooks, there are reports that the government will soon be sending money by check or direct deposit to each of us. The details are still being worked out, but there are a few really important things to know, no matter what this looks like. Learn More >

https://mp.bank/wp-content/uploads/2019/01/Logo.png00Mark Duffyhttps://mp.bank/wp-content/uploads/2019/01/Logo.pngMark Duffy2020-03-19 10:11:182020-08-18 09:03:39COVID-19: Checks from the Government

The FTC and FDA have jointly issued warning letters to seven sellers of unapproved and misbranded products, claiming they can treat or prevent the Coronavirus. The companies’ products include teas, essential oils, and colloidal silver.

https://mp.bank/wp-content/uploads/2019/01/Logo.png00Mark Duffyhttps://mp.bank/wp-content/uploads/2019/01/Logo.pngMark Duffy2020-03-12 14:57:192020-08-18 09:03:39Scammers are taking advantage of fears surrounding the Corona-virus

You get a call from someone who says she’s from the IRS. She says that you owe back taxes. She threatens to sue you, arrest or deport you, or revoke your license if you don’t pay right away. She tells you to put money on a prepaid debit card and give her the card numbers.

The caller may know some of your Social Security number. And your caller ID might show a Washington, DC area code. But is it really the IRS calling?

No. The real IRS won’t ask you to pay with prepaid debit cards or wire transfers. They also won’t ask for a credit card over the phone. And when the IRS first contacts you about unpaid taxes,

they do it by mail, not by phone. And caller IDs can be faked.

Here’s what you can do:

Stop. Don’t wire money or pay with a prepaid debit card. Once you send it, the money is gone. If you have tax questions, go to irs.gov or call the

IRS at 800-829-1040.

Pass this information on to a friend. You may not have gotten one of these calls, but the chances are you know someone who has.

Please Report Scams

If you spot a scam, please report it to the Federal Trade Commission.

Call the FTC at 1-877-FTC-HELP

(1-877-382-4357) or TTY 1-866-653-4261

Go online: ftc.gov/complaint

Your complaint can help protect other people.

By filing a complaint, you can help the FTC’s investigators identify the imposters and stop them before they can get someone’s hard-earned money. It really makes a difference.

Phishing is a tactic that criminals use to lure and gain access to your personal and business financial information. Criminals send emails on the fly, purporting to be from reputable companies, such as yours, to induce individuals within and outside of your business to reveal personal information such as passwords, account numbers, etc.

Think it won’t happen to you?

According to the FBI’s 2018 Internet Crime Report, Washington State ranked #6 in the count of victims by state; and #13 in total loss by victim per state. Still feeling confident? If you are not worried about potentially losing $64,000, then you have no need to continue to read on.

Last year alone the average loss was $64,000, up from $43,000 the year prior.

So what can you do to help detect, deter and prevent yourself from becoming a statistic?

First and foremost, before you act and respond to any email, make certain that the email came from a correct and authorized sender before you send a wire, change a payroll account, pay an invoice, purchase gift cards, etc.

According to the FBI, Business Email Compromise is significantly on the rise. This type of scam targeting companies who conduct wire transfers, have suppliers abroad and do direct deposit payroll. Corporate or publicly available email accounts of executives or high-level employees related to finance or involved with wire transfer payments are either spoofed or compromised through keyloggers or phishing attacks to do fraudulent transfers. Some of the sample email messages have a subject line containing words such as urgent, direct deposit, request, payment, transfer, among others. Based on FBI, there are 5 types of BEC scams:

The Bogus Invoice Scheme- Companies with foreign suppliers are often targeted with this tactic, wherein attackers pretend to be the suppliers requesting fund transfers for payments to an account owned by fraudsters.

CEO Fraud- Attackers pose as the company CEO, business owner or executive and send an email to employees in finance, requesting them to transfer money to the account they control.

Account Compromise-An executive, business owner or employee email account is hacked and used to request invoice payments to vendors listed in their email contacts. Payments are then sent to fraudulent bank accounts.

Data Theft- Employees in HR and bookkeeping are targeted to obtain personally identifiable information (PII) or tax statements of employees and executives. Such data can be used for future attacks.

Attorney Impersonation- Attackers pretend to be a lawyer or someone from the law firm supposedly in charge of crucial and confidential matters. Normally, such bogus requests are done through email or phone, and during the end of the business day.

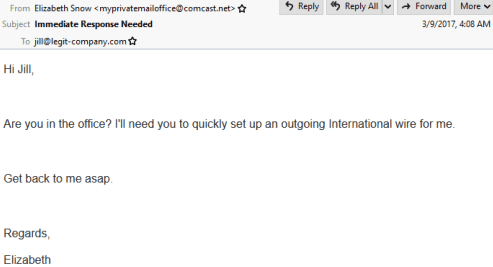

Here is an example of how it works.

The Setup:

The Players

Elizabeth: The CEO being impersonated by the thief. Some simple research is done prior to sending this innocuous email to discover the victim’s name, if they are out of the office and a rough idea of a request that would not raise a red flag.

Jill: The Secondary victim is a key employee of the company, usually in the finance department, that the thief is targeting to enable the fraud to occur. Prior to the setup, research is performed on the target organization to determine whom is enabled to transfer/wire funds.

Thief: the perpetrator in this example. They likely have altered the name displayed in email to match the victim but NOT the actual email address. More skilled criminals will use fake email domain such as @yah00.com instead of @yahoo.com even purchasing the domain to cement their ruse. In very sophisticated attacks, they can spoof or replicate the CEO’s exact email.

The Heist

With Jill believing the email came from the CEO she transfers / wires the money directly to the thief’s account. The best way to avoid being exploited is to verify the authenticity of requests to send money by walking into the CEO’s office or speaking to him or her directly on the phone. Do not rely on email alone.

What can you do? The FBI has issued various tips on how to protect yourself, but one easy way is as follows: have your company start a policy of requiring verbal and/or fax confirmation of all wire transfers. The policy would require the initial written direction be received by email, but before the wire will be initiated your authorized employee would fax and/or call the person directing the wire and receive a secondary verbal confirmation, preferably live confirmation and not simply a voicemail. This may slow down your process, but it will also stop the scam in its tracks. Similar practices can be applied to stop other scams. Such as, if a change to a payroll account is received via email; verbally confirm the request is valid with the employee. If a vendor emails updated payment/invoice information to a new bank and/or bank account; verbally verify with the vendor the change is authentic.

Some other recommendations from the FBI:

Carefully scrutinize all email requests for transfer of funds to determine if the requests are out of the ordinary.

Verify changes in vendor payment location by adding additional two-factor authentication such as having a secondary sign- off by company personnel.

Confirm requests for transfers of funds. When using phone and/or fax verification as part of the two-factor authentication, use previously known numbers, not the numbers provided in the email request.

Conduct employee security awareness training and implement other security protection policies and programs to ensure your business and employees implement and maintain careful business practices to avoid being victims to these and other types of cybercrimes and scams.

Know the habits of your customers, including the details of, reasons behind, and amount of payments.

Create intrusion detection system rules that flag emails with extensions that are similar to company email. For example, legitimate email ofabc_company.com would flag fraudulent email of abc-company.com.

Register all company domains that are slightly different than the actual company domain.

What should you do if you are a victim? If funds are transferred to a fraudulent account, it is important to act quickly:

Contact your financial institution immediately upon discovering the fraudulent transfer.

Request that your financial institution contact the corresponding financial institution where the fraudulent transfer was sent.

Contact your local Federal Bureau of Investigation (FBI) office if the wire is recent. The FBI, working with the United States Department of Treasury Financial Crimes Enforcement Network, might be able to help return or freeze the funds.

File a complaint, regardless of dollar loss, at www.IC3.gov.

Tax Identity Theft Awareness Tax identity theft happens when someone uses your Social Security number (SSN) to get a tax refund or a job. You might find out it’s happened when you get a letter from the IRS saying that more than one tax return was filed with your SSN, or IRS records show you earned income from an employer you don’t know. The IRS may also reject your efiled tax return as a duplicate filing. To help fight tax identity theft: • File your return as early in the tax season as you can. • Use a secure internet connection if you file electronically or mail your tax return from the post office.

Dealing with Tax-Related Identity Theft If the IRS sends a notice or letter saying that someone used your SSN to get a tax refund, or saying there’s another problem, respond quickly and follow the instructions in the letter. • Call the IRS using the telephone number given in the letter. Visit the IRS’s guide, IRS Identity Theft Victim Assistance: How It Works, for more information. • If you think someone used your SSN to file for a tax refund, but you haven’t gotten a letter from the IRS, use IdentityTheft.gov to report it to the IRS and FTC and get a recovery plan. • Visit IdentityTheft.gov to complete an IRS Identity Theft Affidavit (IRS Form 14039) and submit it to the IRS online so that the IRS can begin resolving your case. You’ll also be reporting the identity theft to the FTC.

Other Steps to Repair Identity Theft It is important to limit the potential damage from identity theft. • Put a fraud alert on your credit reports. • Order your free credit reports and close any new accounts opened in your name. • Consider placing a credit freeze on your credit reports.

Follow these tips for hassle-free online shopping: get the details, pay by credit card, keep records, and protect your personal and financial information.

Get the Details

Pay by Credit Card

Keep Records

Protect Your Information

How to Report Online Shopping Fraud

Get the Details

Know who you’re dealing with.

Anyone can set up shop online under almost any name. Confirm the online seller’s physical address and phone number in case you have questions or problems. And if you get an email or pop-up message that asks for your financial information while you’re browsing, don’t reply or follow the link. Legitimate companies don’t ask for information that way.

Know what you’re buying.

Read the seller’s description of the product closely, especially the fine print. Words like “refurbished,” “vintage,” or “close-out” may indicate that the product is in less-than-mint condition, while name-brand items with bargain basement prices could be counterfeits.

Know what it will cost.

Check out websites that offer price comparisons and then compare “apples to apples.” Factor shipping and handling into the total cost of your purchase. Do not send cash or money transfers under any circumstances.

Check out the terms of the deal, like refund policies and delivery dates.

Can you return the item for a full refund if you’re not satisfied? If you return it, who pays the shipping costs or restocking fees, and when you will get your order? A Federal Trade Commission (FTC) rule requires sellers to ship items as promised or within 30 days after the order date if no specific date is promised. Many sites offer tracking options, so you can see exactly where your purchase is and estimate when you’ll get it.

Pay by credit card.

If you pay by credit or charge card online, your transaction will be protected by the Fair Credit Billing Act. Under this law, you can dispute charges under certain circumstances and temporarily withhold payment while the creditor investigates them. In the event that someone uses your credit card without your permission, your liability generally is limited to the first $50 in charges. Some companies guarantee that you won’t be held responsible for any unauthorized charges made to your card online; some cards provide additional warranty, return, and purchase protection benefits.

Keep Records.

Print or save records of your online transactions, including the product description and price, the online receipt, and the emails you send and receive from the seller. Read your credit card statements as you receive them; be on the lookout for charges that you don’t recognize.

Protect Your Information

Don’t email any financial information.

Email is not a secure method of transmitting financial information like your credit card, checking account, or Social Security number. If you begin a transaction and need to give your financial information through an organization’s website, look for indicators that the site is secure, like a URL that begins https (the “s” stands for secure). Unfortunately, no indicator is foolproof; some fraudulent sites have forged security icons.

Check the privacy policy.

Really. It should let you know what personal information the website operators are collecting, why, and how they’re going to use the information. If you can’t find a privacy policy — or if you can’t understand it – consider taking your business to another site that’s more user-friendly.

How to Report Online Shopping Fraud

If you have problems during a transaction, try to work them out directly with the seller, buyer, or site operator. If that doesn’t work, file a complaint with:

the Federal Trade Commission at www.ftc.gov/complaint

your state Attorney General, using contact information at naag.org

your county or state consumer protection agency. Check the blue pages of the phone book under county and state government, or visit consumeraction.gov and look under “Where to File a Complaint.”

Did you recently get a notice that says your personal information was exposed in a data breach?

Did you lose your wallet?

Or learn that an online account was hacked? Depending on the type of information exposed, the Federal Trade Commission can tell you what to do right away. You’ll find these steps – and more – at IdentityTheft.gov/databreach.

What information was lost or exposed?

Social Security number

If a company responsible for exposing your information offers you free credit monitoring, take advantage of it.

Get your free credit reports from annualcreditreport.com. Check for any accounts or charges you don’t recognize.

Consider placing a credit freeze. A credit freeze makes it harder for someone to open a new account in your name.

If you decide not to place a credit freeze, at least consider placing a fraud alert

Try to file your taxes early – before a scammer can. Tax identity theft happens when someone uses your Social Security number to get a tax refund or a job.

Online login or password

Log in to that account and change your password. If possible, also change your username

If you can’t log in, contact the company. Ask them how you can recover or shut down the account.

If you use the same password anywhere else, change that, too.

Is it a financial site, or is your credit card number stored? Check your

account for any charges that you don’t recognize.

Bank account, credit, or debit card information

If your bank information was exposed, contact your bank to close the account and open a new one.

If credit or debit card information was exposed, contact your bank

Information obtained from | Federal Trade Commission | consumer.gov

The IRS, the states and the tax industry are committed to protecting you from identity theft. We’ve strengthened our partnership to fight a common enemy – the criminals – and to devote ourselves to a common goal – serving you. Working together, we’ve made many changes to combat identity theft, and we are making progress. However, cybercriminals are constantly evolving, and so must we. The IRS is working hand-in-hand with your state revenue officials, your tax software provider and your tax preparer. But, we need your help. We need you to join with us. By taking a few simple steps, you can better protect your personal and financial data online and at home.

Please consider these steps to protect yourselves from identity thieves:

Keep Your Computer Secure

• Use security software and make sure it updates automatically; essential tools include:

Firewall

Virus/malware protection

File encryption for sensitive data

• Treat your personal information like cash, don’t leave it lying around • Check out companies to find out who you’re really dealing with • Give personal information only over encrypted websites – look for “https” addresses • Use strong passwords and protect them • Back up your files

Avoid Phishing and Malware

• Avoid phishing emails, texts or calls that appear to be from the IRS and companies you know and trust, go directly to their websites instead • Don’t open attachments in emails unless you know who sent it and what it is • Download and install software only from websites you know and trust • Use a pop-up blocker • Talk to your family about safe computing

Protect Personal Information

Don’t routinely carry your social security card or documents with your SSN. Do not overshare personal information on social media. Information about past addresses, a new car, a new home and your children help identity thieves pose as you. Keep old tax returns and tax records under lock and key or encrypted if electronic. Shred tax documents before trashing.

Avoid IRS Impersonators. The IRS will not call you with threats of jail or lawsuits. The IRS will not send you an unsolicited email suggesting you have a refund or that you need to update your account. The IRS will not request any sensitive information online. These are all scams, and they are persistent. Don’t fall for them. Forward IRS-related scam emails to phishing@irs.gov. Report IRS-impersonation telephone calls at www.tigta.gov.

Additional steps:

• Check your credit report annually; check your bank and credit card statements often; • Review your Social Security Administration records annually: Sign up for My Social Security at www.ssa.gov. • If you are an identity theft victim whose tax account is affected, review www.irs.gov/identitytheft for details.

Information obtained from Department of the Treasury Internal Revenue Service | www.irs.gov | Publication 4524

https://mp.bank/wp-content/uploads/2019/01/Logo.png00Mark Duffyhttps://mp.bank/wp-content/uploads/2019/01/Logo.pngMark Duffy2019-02-02 23:13:002020-08-18 09:03:52Security Awareness For Taxpayers | 1/24/2018

The Federal Trade Commission (FTC), the nation’s consumer protection agency, is warning consumers to be on the alert for scam artists posing as debt collectors.

The Federal Trade Commission (FTC), the nation’s consumer protection agency, is warning consumers to be on the alert for scam artists posing as debt collectors. It may be hard to tell the difference between a legitimate debt collector and a fake one. Sometimes a fake collector may even have some of your personal information, like a bank account number. A caller may be a fake debt collector if he:

is seeking payment on a debt for a loan you do not recognize;

refuses to give you a mailing address or phone number;

asks you for personal financial or sensitive information; or

exerts high pressure to try to scare you into paying, such as threatening to have you arrested or to report you to a law enforcement agency.

If you think that a caller may be a fake debt collector

Ask the caller for his name, company, street address, and telephone number. Tell the caller that you refuse to discuss any debt until you get a written “validation notice.” The notice must include the amount of the debt, the name of the creditor you owe, and your rights under the federal Fair Debt Collection Practices Act. If a caller refuses to give you all of this information, do not pay! Paying a fake debt collector will not always make them go away. They may make up another debt to try to get more money from you.

Stop speaking with the caller. If you have the caller’s address, send a letter demanding that the caller stop contacting you, and keep a copy for your files. By law, real debt collectors must stop calling you if you ask them to in writing.

Do not give the caller personal financial or other sensitive information. Never give out or confirm personal financial or other sensitive information like your bank account, credit card, or Social Security number unless you know whom you’re dealing with. Scam artists, like fake debt collectors, can use your information to commit identity theft – charging your existing credit cards, opening new credit card, checking, or savings accounts, writing fraudulent checks, or taking out loans in your name.

Contact your creditor. If the debt is legitimate – but you think the collector may not be – contact your creditor about the calls. Share the information you have about the suspicious calls and find out who, if anyone, the creditor has authorized to collect the debt.

Report the call. Contact the FTC and your state Attorney General’s office with information about suspicious callers. Many states have their own debt collection laws in addition to the federal FDCPA. Your Attorney General’s office can help you determine your rights under your state’s law.

Information obtained from | Federal Trade Commission | consumer.gov

The FDIC often hears from bank customers who believe they may be the victims of financial fraud or theft, and our staff members provide information on where and how to report suspicious activity. To help further, FDIC Consumer News includes crime prevention tips in practically every issue. As part of that coverage, we feature here a list of 10 scams that you should be aware of, plus key defenses to remember.

Government “imposter” frauds: These schemes often start with a phone call, a letter, an email, a text message or a fax supposedly from a government agency, requiring an upfront payment or personal financial information, such as Social Security or bank account numbers.

“They might tell you that you owe taxes or fines or that you have an unpaid debt. They might even threaten you with a lawsuit or arrest if you don’t pay,” said Michael Benardo, manager of the FDIC’s Cyber Fraud and Financial Crimes Section. “Remember that if you provide personal information it can be used to commit fraud or be sold to identity thieves. Also, federal government agencies won’t ask you to send money for prizes or unpaid loans, and they won’t ask you to wire money to pay for anything.”

Debt collection scams: Be on the lookout for fraudsters posing as debt collectors or law enforcement officials attempting to collect a debt that you don’t really owe. Red flags include a caller who won’t provide written proof of the debt you supposedly owe or who threatens you with arrest or violence for not paying.

Fraudulent job offers: Criminals pose online or in classified advertisements as employers or recruiters offering enticing opportunities, such as working from home. But if you’re required to pay money in advance to “help secure the job” or you must provide a great deal of personal financial information for a “background check,” those are red flags of a potential fraud.

Another variation on this scam involves fake offers of part-time jobs as “mystery shoppers,” who are people paid to visit retail locations and then submit confidential reports about the experience. In an example of the fraudulent version, your job might be to receive a $500 check, go “undercover” to your bank, deposit the check into your account there, and then report back about the service provided. But you also would be instructed to immediately wire your new “employer” $500 out of your bank account to cover the check you just deposited. Days later, the bank will inform you that the check you deposited is counterfeit and you just lost $500 to thieves. One warning sign of this type of scam is that the potential employer requires you to have a bank account.

“Phishing” emails: Scam artists send emails pretending to be from banks, popular merchants or other known entities, and they ask for personal information such as bank account numbers, Social Security numbers, dates of birth and other valuable details. The emails usually look legitimate because they include graphics copied from authentic websites and messages that appear valid.

“We have also seen emails with links to fake websites that are exact copies of real websites for FDIC-insured banks, except the web addresses are slightly different than the real ones,” said Doreen Eberley, director of the FDIC’s Division of Risk Management Supervision, which is in charge of the agency’s policies and programs related to financial crimes. “These sites are used to trick people into giving up valuable personal information that can be used to commit identity theft.”

Mortgage foreclosure rescue scams: Today, many homeowners who are struggling financially and risk losing their homes may be vulnerable to false promises to refinance a mortgage under better terms or rates. But borrowers should always be on the lookout for scammers who falsely claim to be lenders, loan servicers, financial counselors, mortgage consultants, loan brokers or representatives of government agencies who can help avoid a mortgage foreclosure and offer a great deal at the same time. These criminals will present homeowners with what sounds like the life-saving offer they need. Instead, the homeowner is required to pay significant upfront fees or, even worse, tricked into signing documents that, in the fine print, transfer the ownership of the property to the criminal involved. Common warning signs of fraudulent mortgage assistance offers include a “guarantee” that foreclosure will be avoided and pressure to act fast.

Lottery scams: You might be told you won a lottery (typically one that you never entered) and asked to first send money to the “lottery company” to cover certain taxes and fees. Similar examples involve bogus prize winnings and sweepstakes. “In one example, a scammer sent a letter to people using falsified FBI and FDIC letterhead telling them they won a popular, well-known lottery but that they needed to send money by wire transfer to a lottery ‘official’ in order to secure the winnings,” Benardo said. “The ‘official’ was really a crook hoping to trick people into sending money.”

Elder frauds: Thieves sometimes target older adults to try to cheat them out of some of their life savings. For example, telemarketing scams may involve sales of bogus products and services that will never be delivered. Warning signs include unsolicited phone calls asking for a large amount of money before receiving the goods or services, and special offers for senior citizens that seem too good to be true, like an investment “guaranteeing” a very high return. To help seniors and their caregivers avoid financial exploitation, the FDIC and the Consumer Financial Protection Bureau have developed Money Smart for Older Adults, a curriculum with information and resources (see our News Briefs).

Overpayment scams: This popular scam starts when a stranger sends a consumer or a business a check for something, such as an item being sold on the internet, but the check is for far more than the agreed-upon sales price. The scammer then tells the consumer to deposit the check and wire the difference to someone else who is supposedly owed money by the same check writer. In a few days, the check is discovered to be a counterfeit, and the depositor may be held responsible for any money wired out of the bank account. Victims may end up owing thousands of dollars to the financial institution that wired the money, and sometimes they’ve also sent the merchandise to the fraud artists, too.

“Ransomware”: This term refers to malicious software that holds a computer, smartphone or other device hostage by restricting access until a ransom is paid. The most common way ransomware and other malicious software spreads is when someone clicks on an infected email attachment or a link in an email that leads to a contaminated file or website. Malware also can spread across a network of linked computers or be passed around on a contaminated storage device, such as a thumb drive.

Jury duty scams: A thief makes phone calls pretending to be a law enforcement official warning innocent people that they failed to appear for jury duty and threating an arrest unless a “fine” is paid immediately. And to pay up, the caller asks for debit account and PIN numbers, allowing the perpetrator to create a fake debit card and drain the account.

What You Can Do: Plus the basics on how to protect your personal information and your money

While we have described many forms of financial scams, the red flags to look out for are often similar. And so are the things you can do to help protect yourself and your money. Here are some basic precautions to consider, especially when engaging in financial transactions with strangers through email, over the phone or on the internet.

Avoid offers that seem “too good to be true.” As Eberley noted: “If someone promises ‘opportunities’ that are free or with surprisingly low costs or high returns, it is probably a scam. Be especially suspicious if someone pressures you into making a quick decision or to keep a transaction a secret.”

No matter how legitimate an offer or request may look or sound, don’t give your personal information, such as bank account information, credit and debit card numbers, Social Security numbers and passwords, to anyone unless you initiate the contact and know the other party is reputable.

Remember that financial institutions will not send you an email or call to ask you to put account numbers, passwords or other sensitive information in your response because they already have this information. To verify the authenticity of an email, independently contact the supposed source by using an email address or telephone number that you know is valid.

Be cautious of unsolicited emails or text messages asking you to open an attachment or click on a link. This is a common way for cybercriminals to distribute malicious software, such as ransomware. Be especially cautious of emails that have typos or other obvious mistakes.

Use reputable anti-virus software that periodically runs on your computer to search for and remove malicious software. Be careful if anyone (even a friend) gives you a thumb drive because it could have undetected malware, such as ransomware, on it. If you still want to use a thumb drive from someone else, use the anti-virus software on your computer to scan the files before opening them.

Don’t cash or deposit any checks, cashier’s checks or money orders from strangers who ask you to wire any of that money back to them or an associate. If the check or money order proves to be a fake, the money you wired out of your account will be difficult to recover.

Be wary of unsolicited offers “guaranteeing” to rescue your home from foreclosure. If you need assistance, contact your loan servicer (the company that collects the monthly payment for your mortgage) to find out if you may qualify for any programs to prevent foreclosure or to modify your loan without having to pay a fee. Also consider consulting with a trained professional at a reputable counseling agency that provides free or low-cost help. Go to the U.S. Department of Housing and Urban Development website for a referral to a nearby housing counseling agency approved by HUD or call 1-800-569-4287.

Monitor credit card bills and bank statements for unauthorized purchases, withdrawals or anything else suspicious, and report them to your bank right away.

Periodically review your credit reports for signs of identity theft, such as someone obtaining a credit card or a loan in your name. By law, you are entitled to receive at least one free credit report every 12 months from each of the nation’s three main credit bureaus (Equifax, Experian and TransUnion). Start at AnnualCreditReport.com or call 1-877-322-8228. If you spot a potential problem, call the fraud department at the credit bureau that produced that credit report. If the account turns out to be fraudulent, ask for a “fraud alert” to be placed in your file at all three of the major credit bureaus. The alert tells lenders and other users of credit reports that you have been a victim of fraud and that they should verify any new accounts or changes to accounts in your name.

Contact the FDIC’s Consumer Response Center (CRC) if you have questions about possible scams or you are the victim of a scam experiencing difficulty resolving the issue with a financial institution. The CRC answers inquiries about consumer protection laws and regulations and conducts thorough investigations of complaints about FDIC-supervised institutions. If the situation involves a financial institution for which the FDIC is not the primary federal regulator, CRC staff will refer the matter to the appropriate regulator. Visit our webpage on submitting complaints or call 1-877-ASK-FDIC (1-877-275-3342) Monday – Friday, 8am to 8pm (EST).

https://mp.bank/wp-content/uploads/2019/01/Logo.png00Mark Duffyhttps://mp.bank/wp-content/uploads/2019/01/Logo.pngMark Duffy2019-02-02 23:11:542025-06-25 12:01:1810 Scams Targeting Bank Customers: Plus the basics on how to protect your personal information and your money | 6/9/2017

You are about to leave the Mountain Pacific Bank website. By clicking “Continue”, you will be taken to a third party website. Third party websites are not operated by Mountain Pacific Bank, and may not follow the same privacy, security or accessibility standards as those of the Mountain Pacific Bank site.